Entrepreneur and Business Resources

Integral Methods and Technology

Governance and Investor Responsibility

archive

signup

credits

archive

signup

credits

Private and Confidential

September 2005

- Perspective

- Investment, finance & VC * Interest rates and currencies * Trade & FDI

- Activities, Books and Gatherings

The following sections are now delivered through Astraea. The links below will take you to those sections.

Ch...ch...ch...changes!

Perspective

Ray Kurzweil is a leader in articulating the increasing rate of technology change and its impacts. He himself has been part of this revolution as an inventor of speech recognition, scanners, music synthesizers and more: http://www.kurzweilai.net. Kurzweil's Law of Accelerating Returns says that in an evolutionary process, positive feedback increases order exponentially. A correlate is that the "returns" of an evolutionary process (such as the speed, cost-effectiveness, or overall "power" of a process) increase exponentially over time -- in a range of fields including biology, physics, chemistry and psychology. Technology, like any evolutionary process, builds on itself. And in his new book "The Singularity is Near" he makes a strong argument that technology will itself become intelligent within 3 to 5 decades. "The paradigm shift rate (i.e., the overall rate of technical progress) is currently doubling (approximately) every decade; that is, paradigm shift times are halving every decade (and the rate of acceleration is itself growing exponentially). So, the technological progress in the twenty-first century will be equivalent to what would require (in the linear view) on the order of two hundred centuries. In contrast, the twentieth century saw only about twenty-five years of progress (again at today's rate of progress) since we have been speeding up to current rates. So the twenty-first century will see almost a thousand times greater technological change than its predecessor." While we see some critical limitations to his extrapolative thinking (systems generally follow an S curve and we may be at the bottom curve, ie accelerating, but that will level off naturally), the sound research and experience foundation of his view underlies the fact that the "rate of change" is accelerating in a logarithmic fashion and will do so for the coming generation.

Evidence of the acceleration of change in natural phenomena is also rising. The section on climate change below alerts us to the fact that Arctic ice melt rate is accelerating and the ability of plants to be a net absorber of CO2, a greenhouse gas, is waning because climate temperatures are rising too fast.

This requires a fundamental paradigm shift in human thinking. Our way of life is built on the status quo - history is the window to the future. But this is now being undermined. At the first level of change this may simply mean new technology disrupting social and economic models, for which we will find new models. But if the change is accelerating in this logarithmic fashion, the foundation of reason may become a moveable reference because natural systems change their laws constantly. This resonates well with the biology of emerging intelligences. It is clear that humans will think differently in one or few generations.

Today, in order to succeed in this changing world, leaders must think differently: they must think about a lot more dimensions and in a shorter time frame. Resorting to institutional logic will not solve the challenges of today. The following informal opinion from a private think tank illustrates the tension in our global powerhouse America where this challenge is immediate:

Americans invented the telephone, the atomic bomb, and the silicon wafer, and they put a man on the moon, but a very simple scientific fact eludes many of them -- not for 270,000 years has there been as much carbon dioxide in the atmosphere as there is now (~380 parts per million). An atmosphere that traps more heat holds more moisture and produces more frequent extreme-weather events. A 12-year-old could understand this. ... The end run of September 11 was the Iraq war. Will the end run of Katrina be more intensive U.S. oil exploration and fossil-fuel burning? [We] may one day thank the 2005 hurricane season for thwarting the economic arguments against climate action and security. [Ignoring] global warming really is worse than trying to do something about it.

How do we begin to deal with these challenges which seem to have no solution?

Integral thinking is the leading solution to the challenge and it is therefore a prudent investment to develop this skill. Unfortunately, it is an emerging science (in whose application we specialise as you, dear reader, will know) which has yet to be adopted by most leading businesses, nations and organisations. And you have to look carefully to find academic institutions which are applying it - although a number of top executive education organisations are establishing partnerships to develop courses. A basic model of integral systems analysis is available here. The underlying approach is founded in natural science and reflects natural systems - flexibility, robustness. The principle is to analyse situations and organise solutions reflecting a whole system approach. This incorporates three main spheres physical, intellectual, ethical along a spectrum of emerging intelligence from basic needs (like shelter, or sales), through more complex needs (like organisation and communication) to whole system needs (like equity). Fortunately integral thinking is innate in all of us though generally repressed by traditional education and institutions, and can be liberated in a reasonable time frame. We are also in the age in which it is emerging. An example of integral thinking is the web: a self organising, non-hierarchical reflection of all members' (users) needs.

Investment, Finance & V. C.

The global financial climate has not improved. The shift of savings from Asia to US has continued. American savings rate remains in a trough. Asian saving rates are high and these savings are backing the purchase of dollars. But the imbalance will not continue for long. Greenspan gives us the big picture: "History has not dealt kindly with the aftermath of protracted periods of low risk premiums". While interest rates remain modest we must be in one of the most volatile periods of economic history. Risk levels have been raised by the Iraq war (in an age when military action is generally declining), climate change now causes unforeseen risks like Katrina, fires in Portugal and floods in central Europe and China, industrial business cycles have been shortened by the pace of technological change, and consumer behaviour has become sophisticated and flexible because of internet information flows and transaction processing. Assets and people exposed to risk are also greater than ever before. There are a number of pressure valves which can release tension, but all are dependent on multilateral agreement and action, which requires compromise even from America. Sentiment will keep the market buoyant till January, but strategic planning for 2006 should consider that global economic imbalances will seek equilibrium soon.

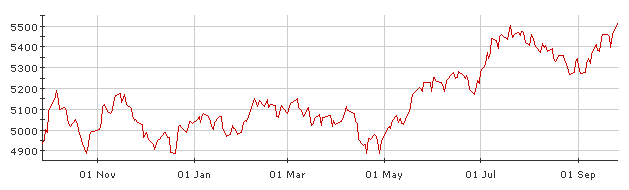

Stock

market performance has been good over the past year as the BBC

global 30 indicates. But successful portfolios are more likely

to have picked low risk stocks as unexpected developments across sectors

occur, from insurance to commodities to pharma.

Stock

market performance has been good over the past year as the BBC

global 30 indicates. But successful portfolios are more likely

to have picked low risk stocks as unexpected developments across sectors

occur, from insurance to commodities to pharma.

Weather-related insured losses have grown 15 times larger over the last 30 years, according to a new report. Availability and Affordability of Insurance Under Climate Change, commissioned by advocacy group Ceres, notes that if present trends continue, climate change could make insurance unavailable or unaffordable for businesses and consumers. Mindy Lubber, Ceres president. "Insurers and regulators have failed to adequately plan for these escalating weather events that scientists predict will intensify in the years ahead due to global warming." Consumers in the US face higher premiums, lowered limits and increased coverage restrictions thanks to recent weather-related losses, even before the devastation wrought by Hurricane Katrina in New Orleans, according to the report. For example, seven private insurance companies stopped providing homeowner insurance in Florida after last year's string of hurricanes, leaving the state as insurer of last resort, incurring $2.5 billion in losses. The report also notes that weather-related losses in the US have grown from "a few billion dollars a year in the 1970s to an average of $15 billion a year in the past decade." And this growth is 10 times faster than rises in insurance premiums since 1971.

Employer-sponsored health insurance is becoming scarcer and more costly according to the annual health coverage survey conducted by the Kaiser Family Foundation and Health Research & Educational Trust. Their report shows that premiums for job-based health insurance is rising 9.2 percent on average nationwide in 2005, about three times the general rate of inflation. More worrying, the slice of companies providing health benefits to employees has dropped to 60 percent in 2005, down from 69 percent in 2000.

US consumer spending fell 0.5% in August - the largest monthly fall in nearly four years - reflecting the recent rise in gasoline and domestic fuel prices. Petrol climbed above $3 a gallon for the first time after Hurricane Katrina. And the government estimated that the hurricane destroyed uninsured property worth $100billion in four Southern states. Consumer confidence, as surveyed by the University of Michigan, dropped by more than expected in September. The index of consumer sentiment dropped to 76.9 in September, from 89.1 in August, the biggest drop in two years. The Conference Board's Consumer Confidence Index sank 18.9 points to 86.6 from a revised 105.5 in August. Figures also showed a 0.1% fall in personal incomes, due largely to damage wrought by Katrina. When adjusted for inflation, consumer expenditure dropped 1%, the steepest monthly fall since the 11 September 2001 attacks. The higher cost of fuel also pushed up consumer inflation, which rose 0.5% last month. Other figures showed sales of new houses fell in August by their greatest amount in nine months - by a greater than expected 9.9%,however the rate was still 6.2% higher than a year previously, and prices were up 2.5% on July's rate to $220,300.

While the German economy is moving in the right direction, a new concern is rising. 1/7 of German labour is connected to the auto industry which is being forced to rebuild itself by the higher cost of oil and the availability of alternative fuels and transport systems. Nevertheless, it is likely that Germany will manage the change well because there is already a strong foundation of new thinkers. The German industry is more able to restructure itself to serve the new consumer and energy demands and business structures.

Japan's

economy continues to move in the right direction. In August

industrial output rebounded during the month, rising 1.2% in August from

July. Unemployment rate fell to 4.2% in August, from 4.4% in July, raising

hopes that an increase in the workforce could eventually lead to higher

consumer spending. Separate government figures showed that spending

by households headed by salaried workers rose by 3.2% in August from July.

Overall consumer spending accounts for about 55% of the Japanese economy.

Japan's

economy continues to move in the right direction. In August

industrial output rebounded during the month, rising 1.2% in August from

July. Unemployment rate fell to 4.2% in August, from 4.4% in July, raising

hopes that an increase in the workforce could eventually lead to higher

consumer spending. Separate government figures showed that spending

by households headed by salaried workers rose by 3.2% in August from July.

Overall consumer spending accounts for about 55% of the Japanese economy.

The general improvement seen this year have led to prospects that are better than for a very long time for an increase in Japanese institutional weightings to domestic equities. In the longer term, the case for an asset-allocation switch to equities in Japan remains strong given the demographic profile.

UNCTAD's World Investment Report 2005 presents the latest trends in foreign direct investment (FDI) and explores the internationalization of research and development by transnational corporations (TNCs) along with the development implications of this phenomenon.

A recent report illustrates the scale of corruption in China. Many Chinese officials and bankers have escaped prosecution by fleeing abroad with large sums of money, often to other parts of Asia or to North America. The Ministry of Commerce has estimated that 4,000 corrupt officials have fled the country with roughly $50billion in the past two decades.

The Pollution Control Board of Kerala in India has ordered

Coca Cola to close its major bottling plant with immediate

effect. The move comes after several years of protests against the plant

by local campaigners. Villagers in the nearby areas had accused Coke of

depleting local groundwater, and producing other local pollution. The

controversy has received considerable coverage and become a cause celebre

for anti-corporate activists. It is another illustration of "Enron" risk

- unethical behaviour by business leaders resulting in loss of reputation,

business and assets.

We are researching micro finance

with a view to investment. Our working notes are being uploaded

here.

Responsible Investing

Carbon Disclosure Project (CDP), an initiative backed by institutional investors controlling more than $ 21 trillion (£12 trillion) of assets, warns there is a huge and worrying gap between awareness among big companies of the risks posed by climate change and action to combat it. According to the report fewer than one in seven of the world's top 500 companies by market capitalisation has reduced carbon emissions in the past year and in more than one-sixth of cases emissions have gone up. In the most extreme circumstances the cost of meeting tougher curbs on carbon emissions could wipe as much as 45 per cent from the annual profits of some companies such as big American power producers. Steel and mining companies could see reductions in earnings of as much as 20 per cent while the chemicals sector could face annual compliance costs equal to nearly 4 per cent of net profits. Included in the 'blacklist' of companies that failed or declined to participate in the survey are Boeing, Home Depot, Wal-Mart, Apple, News Corporation and Carnival. Nearly half those surveyed refused to disclose any emissions data. CDP signatories have significantly increased from CDP2, when 95 institutional investors representing $10 trillion in assets signed on, to 155 signatories with $21 trillion in assets in CDP3. Most of the world's biggest companies are failing to cut their carbon emissions even though the long-term cost of complying with tougher rules to tackle global warming could have a devastating impact on their profitability.

Imperial Chemical Industries and the two German chemical groups BASF and Degussa have the edge over their competitors in the chemical industry when it comes to acting responsibly toward society and the environment, according to a recent industry survey. The rating agency oekom research took a close look at 23 companies from nine countries and, against almost 200 criteria, assessed how they cope with social challenges and environmental risks. On average, the companies achieve higher ratings on social issues than on environmental issues. The analysts are critical above all of the generally poor efforts to record and evaluate substance risks or to develop environmentally sustainable replacement substances. oekom research acknowledges, on the other hand, that the entire industry has made significant progress in areas which have been focal points of public concern for many years, for example in occupational safety or in plant and transport safety.

Fortune magazine has announced the results of its 2005 Accountability Rating, a rating of corporate responsibility of Fortune Global 100 companies. The Accountability Rating -- compiled by the London think tank AccountAbility and the consultancy CSRnetwork -- scores companies on how seriously their future decisions will consider nonfinancial matters. Topping the survey is BP, followed by Royal Dutch Shell Group (No. 2); Vodafone (No. 3); HSBC Holdings (No. 4); Carrefour (No. 5); Ford Motor (No. 6); Tokyo Electric Power (No. 7); Electricitede France (No. 8); Peugeot (No. 9); and Chevron (No. 10). The Accountability Rating is not an index of how much good the company does or how loud its critics are. "It doesn't seek to label the good or bad but rather to identify the smart," says Simon Zadek, chief executive of AccountAbility. "It's a business, not a moral, rating. It looks at the world's biggest corporations and asks, 'Do they understand how to create and exploit effective business opportunities by addressing the needs of the poor? Do they understand how to make money by investing in environmentally sound business practices? Are they, in short, prepared to maximize the opportunities for our changing world? It will be interesting to see which corporations get smart first in aligning their business strategies to emerging social and environmental risks and opportunities," concludes Zadek. "One thing is clear: Those that will not or cannot change their strategies will ultimately not maintain their rankings in the Fortune Global 100."

Ford seems to be a bit mixed up. On the one hand they invest in top advice from people like Bill McDonagh and Michael Braungart on organisation and infrastructure design and aim for a 10x increase in hybrid cars by 2010. William Ford even joined over 20 global corporate leaders in calling publicly for George Bush and the G8 to set climate-stabilisation targets and adopt cap-and-trade or other market-based mechanisms. But then they decide to fire 10,000 people because they can not think of a better option! They also agreed to sell rental car giant Hertz Corp. for $ 1.5 billion to private equity firms Clayton, Dubilier & Rice (CD&R), Carlyle Group and Merrill Lynch Global Private Equity.

The following hedge fund story is simply an illustrated warning "caveat emptor". The founder and chief executive of US hedge fund Bayou Group have pleaded guilty to a fraud which allegedly cost investors millions of dollars. Chief executive Samuel Israel and the fund's head of finance Daniel Marino admitted to defrauding investors by misrepresenting the value of the fund. They admitted reporting false rates of return on the fund as well as creating a phoney accounting firm as a cover. Bayou is the latest in a growing number of frauds involving hedge funds which are largely unregulated and traditionally serve institutions and wealthy investors - in the last five years, US regulators have unearthed 51 cases involving hedge fund advisers who have defrauded investors to the tune of $1 billion.

Richard Reed, founder and public face of smoothie brand, Innocent,

is one of the 10 finalists short listed for the UK's 2005 Grocer Cup,

awarded to leading industry figures for Outstanding Business Achievement.

Up against supermarket tycoons, such as Tesco’s chief executive, Sir

Terry Leahy, and Sainsbury’s chief executive, Justin King, Reed has

been praised for having “carved out a profitable niche” for innovative

brand Innocent, within the highly competitive drinks market.

Peter Kinder of KLD Research has released a paper

on the evolving SRI world, including a study of the language used

and its interpretation. It builds on some of the remarks made

by Paul Hawken that started a critical self review in the industry at

the end of last year. It also highlights the rapid pace of change

(another case supporting our perspective of accelerating change) in

investment behaviour.

SRI Notes and SRI-Extra, are two weblogs (or "blogs") devoted to SRI that have sprung up in the past year. They include topics such as a discussion tying game theory to socially responsible business practices, a review corralling recent developments on divestment from companies doing business with the genocidal government of Sudan and links to online resources on socially responsible investing (SRI) and corporate social responsibility (CSR).

Venture Capital

Almost everyone attending the Asian Venture Capital Journal forum had a comment about the huge buyout funds being raised in Asia, and a lack of deals to sustain the investments by those funds. Most of the attendees voiced concerns that these new funds are bidding up prices for deals in North Asia and India, and suggested the real problems may begin if a shortage of high-quality deals in those areas causes the large private equity players to fly into Southeast Asia to bid on the more visible deals. There was also concern that government investors have the ability to muddy waters further by their overbidding. Many think that the disparate markets in the region, the different languages and cultures, and the small size of the deals here, in both venture and buyouts, will prohibit the major firms without in-country staff from taking part in the most lucrative investment opportunities, but that does not mean they will not try to get in on the bidding game. And despite the problems caused by government regulatory intervention and other problems in markets such as Indonesia, Thailand and Vietnam, almost every speaker had positive deals to report over the past year.

While investors have justifiable concerns about these new funds, especially in Asia − where Affinity, Blackstone, Carlyle, CVC, KKR, Newbridge and now JP Morgan Partners Asia all have billion-dollar funds − they're still signing up for these funds with little restraint, pushing fund managers to take even more. It's turning the private equity environment in Asia into a pretty worrying place, where 20 and 30-something-year-old entrepreneurs and VCs suddenly have seven to eight-figure expectations for even the most unlikely business investments. We've seen it before and can only recommend care and pragmatism because even the best get burned in this kind of environment.

A China Venture Capital year book is now available, which includes:

-

More than 900 pages with over 400 easy reading charts & table

-

Full coverage of official policies, laws & regulations on venture capital in China

-

Independent reports on trend & prospect of China's venture capital markets & industry

-

Comprehensive statistical surveys of 144 venture capital firms from China's 24 regions

-

In-depth analysis of China's industries

-

Insightful research of venture capital hot issues in China

-

13 case studies on venture capital investments in China

-

Useful industry directory

For inquiries, please e-mail zhengwenfu@hotmail.com or call +8610-86426850

Interest Rates and Currencies

US Interest rates continue their rise as expected.

The possibility of a pause to breath for Katrina and Rita was not necessary

because of spending to rejuvenate affected areas. The concerns

about housing bubbles, inflation and government finances continue.

The chart to the right illustrates the decline of the dollar and its

current low level compared with the import price index, which has naturally

risen as the dollar has weakened. Normal equilibrium tendency

suggests that the dollar should appreciate, but it is being held back.

The imported inflation may be an increasing concern as America is increasingly

a service economy, importing manufactured goods. It may also be

that the low dollar value and rising interest rates underpin the investment

strategy of other central banks - "the dollar must appreciate soon so

we should hold dollars and sell them when they are more valuable".

Certainly recent reports and analysis of currency

flows indicate that diversification from US dollars by central banks

and others has not happened this year. At the end of 2004 currency

diversification appeared to be happening, and for sound asset allocation

reasons. However, it has not continued this year and numbers by

IMF indicate that dollar holdings by Asian banks are robust. While

we expect diversification to continue to Euro and local currencies,

it has not been as quick or soon as at first anticipated, and this might

affect short term currency policy. As a medium to long term strategy

it remains appropriate to diversify currency exposure to local currencies

and to balance portfolios with Euros against US Dollars.

The notion that the US$ will lose its status as the world's main

reserve currency has been debated more vigorously recently,

as it is once a decade when the the dollar depreciates. What is

new today is that the Euro is offering a serious alternative because

of its stability and the volume of trade and business denominated in

Euro. While the main reserve currency is not likely to change

for some years, it does appear that prudent central bank policy is to

diversify reserves more to the Euro. This will accelerate over

the coming decade and should form a key part in long term planning.

Trade and FDI

According to the World Investment Report by UNCTAD FDI is up after

falling for three years, as this chart from The

Economist shows.

Following last month's note on Chinese banks some more statistics have arrived on our desk to colour the picture. From 1950 to 2003, foreign banks put a cumulative total of perhaps $ 2 billion into the Chinese banking system. In the past 12 months alone, foreign investors have committed nearly US$20 billion to direct equity stakes in Chinese banks - with more on the way. This figure does not even include another US$20 billion in actual and planned overseas listings. According to optimistic estimates, at this pace foreigners may own as much as one sixth of the entire mainland banking system by 2008. To some observers, this is a historic chance to buy into the greatest growth story in the world. To others, this is a pending disaster for foreign financial institutions. You know which camp our pragmatism puts us in.

A World Bank study Agricultural Trade Reform and the Doha Development Agenda examines why agricultural trade reform is critical to a favourable development outcome from the Doha Development Agenda. It builds up from the essential detail of the tariffs and other protection measures, and uses this information to provide an analysis of the big-picture implications of proposed reforms.

China's surging textile exports to the United States and Europe this year became a hot political issue during August, with Beijing at odds with Washington and Brussels over caps they imposed to protect domestic producers. The following is a summary of the key issues and stances from Reuters:

Global Trade Rules

The disputes stem from the January 1, 2005, expiration of a global quota system limiting textile trade between countries. Without the limits, U.S. and European retailers were free to buy as many garments as they wanted from China. But as part of its entry into the World Trade Organisation in late 2001, China agreed that the United States and Europe would have the right to invoke "safeguard measures" limiting growth in imports from China to 7.5 percent a year through to 2008 if it could be shown that such imports were causing market disruption.

EU

In June, China and the European Union agreed to limit growth in shipments of 10 lines of Chinese textile products to between 8.5 and 12 percent a year. But the quotas for 2005 were quickly filled, and 84 million trousers, blouses, and other clothing items are now held up in European ports. European Trade Commissioner Peter Mandelson is in Beijing to try to strike a deal during a summit between European leaders and Chinese President Hu Jintao in Beijing on Monday. Mandelson failed to secure backing in Brussels on Friday for the immediate release of about 80 million bras, sweaters and other goods piled up in ports and warehouses or en route for Europe. Countries with strong retail sectors, such as the Nordic states and Germany, have demanded the swift release of the goods, but face opposition from France, Italy, Spain and Portugal, which are still significant textile producers.

US

China's textile exports to the United States nearly doubled in the

first six months to $7.4 billion, causing alarm in textile-producing

states and heightening fears about the ballooning U.S. trade deficit

with China, which hit a record $162 billion in 2004. Earlier this year,

the Bush administration slapped safeguard curbs

on imports of Chinese-made trousers, shirts, underwear and cotton yarn.

It imposed extra curbs on bras and synthetic fabric last week just hours

after the failure of talks aimed at reaching a comprehensive deal governing

imports.

PRC

China says its textile export growth has been reasonable and stems

from competitive advantage provided by lower wages. It made 17 percent

of the world's clothing in 2003, and the WTO expects that share to climb

to 50 percent by 2008. The sector, which employs 19 million people,

is also an important source of jobs in a country whose Communist rulers

are highly concerned with social stability. In its talks with the European

Union, Beijing has been pushing to

have the quotas raised. In discussions with the United States, it is

seeking a long-term deal that will ensure it does not face future safeguard

measures.

Retailers

Retail associations oppose limits on imports, saying they result in higher prices and hurt consumers. U.S. retailers such as Wal-Mart and Gap Inc. and European ones like Sweden's Hennes and Mauritz and Spain's Inditex all source some clothing from China. The Netherlands, Denmark, Sweden and Finland have warned they face job losses and bankruptcies among retailers unless the curbs are eased. German retailers have raised the prospect of legal action.

Activities, Books and Gatherings

The development of a simple integral modelling tool took a step forward in September. Graphic representation of emerging intelligences fell into place. A basic model is viewable here. Readers will recognise the elements of spiral dynamics, integral thinking, business consciousness and spiritual teaching. It is powerful because it is applicable across industries and sectors, lifestages, individuals and organisations and brings all elements together.

Our rediscovered aqueduct at Ballin Temple was recently covered in a feature in a local newspaper. (It was an unexpected encounter with local journalism.)

I'm afraid I've let Pratchett get the better of me again. Small

Gods is TBL excellent and I'm well through Lords

and Ladies. Pratchett is ahead of his time. I don't

know of any other author that can explore enlightened thinking and philosophy

as a derivative of the narrative of a great story.

Emotional Intelligence deserves

another mention because it has been quite helpful in focusing attention

on personal emotions and managing them. Well recommended.

Our websites have been slightly updated. The principal change has been

to install news feeds on the home page and reorganise site section links

thus making the home page a more useful daily launch pad for surfing.

www.astraea.net has world news,

www.griequity.com has business

news and links to main resources.

Our friend Louise Smart's new website is up: www.emotional-detoxing.com. Louise offers a personal advisory consultancy specifically for senior Executives and Directors whose professional or personal circumstances depend on absolute discretion and trust.

Graham Wilson has shared an eye opening article on Jack Welch's management style. I recommend it to fans of Welch and executives building performance organisations.

Fortune's Formula by William Poundstone tells of a scientific betting system that can beat the market. It describes the story and use of physicists John Kelly's formula which tells you how much to bet based on your edge and the risk profile. It is said to appeal to readers of books like Bernstein's Against The Gods, one of our top recommendations, so its probably worth a look.

French speakers may enjoy www.defipourlaterre.org, an eco website with popular backing which was recommended by one of our friends.

Parents might enjoy Fluffledums a new interactive website which explores challenges of living with nature.

This report has been prepared for information purposes and is not an offer, or an invitation or solicitation to make an offer to buy or sell any securities. This report has not been made with regard to the specific investment objectives, financial situation or the particular needs of any specific persons who may receive this report. It does not purport to be a complete description of the securities, markets or developments or any other material referred to herein. The information on which this report is based, has been obtained from publicly available sources and private sources which may have vested interests in the material referred to herein. Although GRI Equity and the distributors have no specific reasons for believing such information to be false, neither GRI Equity nor the distributors have independently verified such information and no representation or warranty is given that it is up-to-date, accurate and complete. GRI Equity, associates of GRI Equity, the distributors, and/or their affiliates and/or their directors, officers and employees may from time to time have a position in the securities mentioned in this report and may buy or sell securities described or recommended in this report. GRI Equity, associates of GRI Equity, the distributors, and/or their affiliates may provide investment banking services, or other services, for any company and/or affiliates or subsidiaries of such company whose securities are described or recommended in this report. Neither GRI Equity nor the distributors nor any of their affiliates and/or directors, officers and employees shall in any way be responsible or liable for any losses or damages whatsoever which any person may suffer or incur as a result of acting or otherwise relying upon anything stated or inferred in or omitted from this report.