Entrepreneur and Business Resources

Integral Methods and Technology

Governance and Investor Responsibility

archive

signup

credits

archive

signup

credits

Private and Confidential

May 2006

- Perspective

- Investment, finance & VC * Interest rates and currencies * Trade & FDI

- Activities, Books and Gatherings

The following sections are delivered through Astraea. The links below will take you to those sections.

Perspective

I was pulled between the extremes of

optimism and futility in May, even wondering "have I been living

under a stone?". The optimism was engendered by a host of businesses

and projects which are initiating positive change and helping turn humanity

from an exclusive beast to an inclusive part of nature. On the other

hand there were personal and global warnings that we are accelerating

down the wrong road. Could the wars in Iraq and Afghanistan, the

west's growing confrontation with Iran, and efforts to divest North Korea

of its nuclear weapons approach crucial turning points that might

combine to create a perfect storm of simultaneous international crises?

Could the economic rumblings, like the dollar decline, trade imbalances

and inequities and various asset bubbles combine to destabilise our cosy

lifestyles?

On the positive side, BeTheChange in particular introduced some powerful businesses, like Eprida, and change agents, like Stan Thakera and Tim Flannery. These businesses and people will make it possible to recreate humanity such that we see the world though a filter that is more unified and wholesome than the current belligerence in politics and economics. But at the same time it is depressing to hear of ignorance and selfishness among privileged people who imagine that traditionally derived solutions, like Halliburton's Survivaball (see Climate Change section), might work, and, even worse, that we are manipulated by rich power brokers more than we imagine (see Geopolitics).

On a personal note, my predilections to family business were greatly challenged. A number of people I respect denigrated the idea of pursuing family business, although I still maintain the view that family values are appropriate for long term stability of organisations. In one incident, I met a man with 6 siblings who chats with them all weekly, but never wanted to be involved in his father's business and does not want his children to take over his; this carries weight because he has built a billion dollar private business group in which the principals aim to share ownership with management up to 50% - he is extremely successful and fair. I reflected that Einstein, and other greats, never created family legacies. And two family enterprises with which I am in touch appear to be choosing dualistic strategies rather than unified ones. As Pratchett notes "gold and mud come out of the same hole" - that is to say there is no telling what creature your loins will create. The longevity of family businesses (they are the oldest in the world; we have a tenuous 15 generation record) suggests that families can create an environment that nurtures the right kind of guardian, but I've not seen any literature, even supported conjecture, that this might be the case. Perhaps the key is to nurture family values, but allow succeeding generations to adapt to the changing world that organisations inevitably face.

Investment, Finance & V. C.

The big news in May was that markets started to rumble. This would not have been surprising to readers of this newsletter, although timing is always difficult to predict. There seemed to be no particular event that catalysed the sell off in stockmarkets and the dollar, but the weight of imbalances had to be recognised soon. Perhaps it was the classic motto "sell in May and go away" that appealled to investors who have seen attractive gains in portfolios. Perhaps it is the growing realisation that theyre is alot oif liquidity fuelling inflation, and not finding useful investment. Perhaps it was the exhaustion of war. Or the realisation that oil prices are going to remain high and we are passing Hubbert's Peak. What is important is that investors avoid hype and seek value while they can.

China and India are quickly becoming the focii of the global economy depreciating the importance of the US and Europe. The news in the paragraphs below add to this. While it is certain that growth and opportunities are abundant in these Asian economies the outlook is beginning to mature. The May FEER led with an article on China's capital market by a McKinsey director and senior fellow. It is useful in highlighting some of the concerns with which you may be familiar and one statistic that stands out is the decline in investment efficiency: In the early 1990s $ 1 of GDP growth was achieved with $ 3.30 of capital, but since 2001 $1 of growth required $ 4.90 of new investment, which is 40% more than South Korea or Japan during their high growth periods. The deterioration of this relationship is a powerful indicator of what it will take to make investments work in China. With 70% of China's capital stock coming from the banking system and only 15% from equity, there is little flexibility in the system and banking problems will increasingly make planning difficult. Even India has 35% of capital provided by equity, a similar proportion to the US. The pressure for rejuvenation of financial infrastructure in China is high and changes must occur in the next five years if gross imbalances are to be lessened.

This restructuring is already under way. China's state banks face a huge increase in competition from December, when the government will open the retail banking market to overseas lenders who will be able to open their own branches in the country. In anticipation of this the top Chinese banks are raising new capital and taking on partners.

May saw the largest IPO since 2000, and it was in China. The Bank of China raised about $ 9.7 billion, selling nearly 26 billion shares at 38 cents each on the Hong Kong Stock Exchange. The bank had received private equity investments of $ 3 billion for a 10% stake prior to the IPO from The Royal Bank of Scotland, Merrill Lynch, Singapore's Temasek and several high net-worth private investors, including Li-Ka Shing. BoC is the country's second largest lender and has one of the most international outlooks of all China's banks, with offices around the world and a listed subsidiary in Hong Kong. Its position as China's principal foreign exchange bank has also enhanced its profile in the eyes of would-be investors. But some analysts have warned off investors, pointing out the bank's problems with bad loans, fraud investigations and antiquated computer systems. Demand was strong and the sale was oversubscribed as investors placed orders worth $152bn for Bank of China shares, with the retail side at least 70 times over-subscribed. The company priced its shares at 2.95 Hong Kong dollars ($0.38) each, 5 cents below the top of its pricing range. Trading of Bank of China shares starts on 1 June.

The country's largest lender, Industrial & Commercial Bank of China, is planning a $ 10 billion share flotation for later this year.

China drew attention to the issue of bad loans after it forced Ernst & Young to withdraw a report just published which estimated the total exposure of China's financial system to bad loans to be $911bn. That included $358bn - nearly three times the official figure - at the big four state banks. Nine days after it was issued, E&Y withdrew the whole report, saying the $358bn figure was "factually erroneous" and lamenting the absence of the "normal internal review and approval process" before publication, which is probably an exageration at least. The withdrawal was more likely done to protect its China business and mollify the People's Bank of China, the central bank, which had publicly called the report"ridiculous and barely understandable" hours before E&Y backed down.

A general survey on international banking was published by the Economist in May. It discusses the massive size of global banks and the pros and cons of such mega-bank strategies. The report covers both India and China offering a useful summary of issues.

The economy of China continues to be resilient. Chinese retail sales have jumped 13.6% during April, a sign that domestic demand is starting to catch up with the nation's red-hot export sales. There have been concerns that China's boom was too reliant on investment and trade, with consumer spending too weak for it to weather a global slowdown. However, analysts said that retail sales are now likely to keep improving. April's data from the National Bureau of Statistics topped market forecasts, and was up from 13.5% in March.

Anecodtally, a total of 41% of respondents in the BBC World Poll, powered by GMI, had China's economy in top spot by 2026, 35% plumped for the US, 10% chose Japan, and 6% favoured India. The findings contradict a Goldman Sachs projection of the world's economies which had the US in top place in 2026.

Media in India report that Goldman Sachs Group will establish a $1 billion property investment fund for India, becoming the fifth or sixth new real estate fund to be announced for India over the last month. RE Venture Fund Advisors of Mumbai and New Delhi, India, is raising two real estate investment funds for India. RE Capital India Fund I is raising $25 million and RE Capital FDI Fund is raising $100 million to $250 million. The Reserve Bank of India continues to withhold approval of about four dozen foreign private equity real estate investment fund filings due to fears of hyperinflation in India's real estate market.

In India, the stock market dropped significantly in May forcing the Bombay Stock Exchange to halt trading. The previous crash of the BSE, another black Monday in India in 2004, saw a loss of about 450 points. This time one single, intraday drop of over 1,100 points, or almost 10%, followed the previous week's 7% drop.

Bush signed into law a $ 70 billion tax cut which he says will boost the US economy. But analysts say it is a tactical move to help Republicans keep control of Congress in November's mid-terms elections. The cut comes as a poll indicates public confidence in the Republican Party has reached a new low. Bush says his "pro-growth economic policies are working for all Americans". Democrats say the cuts are irresponsible and favour the wealthy. Its provisions include a two-year extension of reduced tax rates for capital gains and dividends, which were set to expire at the end of 2008.

The US economy doesn't seem to need help. It registered 5.3% growth in GDP in the first quarter of 2006, its fastest growth rate in two-and-a-half years, revised official data has shown. The new figure for the first quarter is more than triple the 1.7% growth rate recorded in the last quarter of 2005. The upward revision, from the initial 4.8%, came as growth was led by exports and firms increasing inventories, said the Commerce Department.

America could be better served by an overhaul of the tax system, which was mooted but now seems to be on hold. As far back as1984, The Grace commission encapsulated their findings which, among the shocking things revealed the following: Resistance to additional income taxes would be even more widespread if people were aware that:

-

One-third of all their taxes is consumed by waste and inefficiency in the Federal Government as identified in the survey.

-

Another one-third of all their taxes escapes collection from others as the underground economy blossoms in direct proportion to tax increases and places even more pressure on law abiding taxpayers, promoting still more underground economy - a vicious cycle that must be broken.

-

With two-thirds of everyone's personal income taxes wasted or not collected, 100 percent of what is collected is absorbed solely by interest on the Federal debt and by Federal Government contributions to transfer payments. In other words, all individual income tax revenues are gone before one nickel is spent on the services which taxpayers expect from their Government.

Reflecting the theme of predatory lending covered a couple of months ago, Bernanke tried ot focus the administration of the value of a well educated population, saying that: Financial literacy leads to better decision-making among consumers and to improvement in the financial markets. This was not indicative rhetoric that might be expected in connection with predictions about interest rate movements. Bernanke said clearly that while technology has transformed the ability of the financial services industry to provide a greater range of products to a larger audience, the public still needs the financial knowledge to make informed decisions. He believes that a better-informed public will also promote lower-cost financial products.

Henry "Hank" Paulson, the chairman of investment bank Goldman Sachs, has been nominated as the US treasury secretary. He will take over the role from John Snow, who is resigning after three years in the job. Paulson has been chairman and chief executive of Goldman Sachs since May 1999, when the bank went public. He worked for the White House in a previous life: he was a member of the domestic council as staff assistant to President Nixon in 1972. Is this good news? Despite being an appointee of Bush, it may be: Goldman Sachs has recently promoted its publications on the importance of analysing ESG risks (as reported in the Review of December 2005) and Paulson is reputed to be an avid nature-lover, being chairman of the board of The Nature Conservancy in the US. Paulson also spent most of the most recent Goldman AGM defending their environment policy - well done Hank.

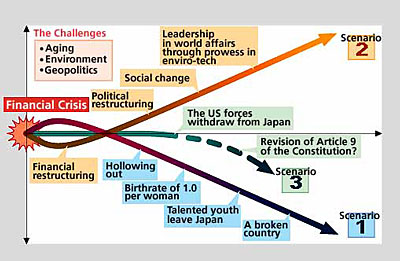

Japan's

performance continues to be better. It appears to be joing the global

habit of inflation. Japanese consumer prices were higher in April

than a year ago, the sixth month in a row they have risen, lifting hopes

that deflation has been shaken off. Japan watchers will be interested

in the scenario

forecasting of Nakamae International Economic Research on possible

courses that Japan could take during the period up to 2010 - 2020. The

scenarios are built around the four key challenges facing Japan: the financial

crisis, the aging of Japan's population, local and global environmental

problems, and changes in existing geopolitical relationships.

Japan's

performance continues to be better. It appears to be joing the global

habit of inflation. Japanese consumer prices were higher in April

than a year ago, the sixth month in a row they have risen, lifting hopes

that deflation has been shaken off. Japan watchers will be interested

in the scenario

forecasting of Nakamae International Economic Research on possible

courses that Japan could take during the period up to 2010 - 2020. The

scenarios are built around the four key challenges facing Japan: the financial

crisis, the aging of Japan's population, local and global environmental

problems, and changes in existing geopolitical relationships.

A new Ceres report, Climate Risk and Energy in the Auto Sector -- Guidance for Investors and Analysts on Key Off-balance Sheet Drivers, finds that the uncertainty in the U.S. regarding the future course of energy and climate change policy is a major problem for investors and Wall Street analysts in assessing the value of auto companies, and that analysts need better disclosure from auto companies about their strategies for managing the risks and capturing the opportunities posed by new energy and climate change policies taking effect worldwide. The Ceres report analyzes several key trends that could affect the valuation of auto companies' securities, which are already subject to critical scrutiny. Three conclusions were widely agreed upon by the analysts at the meeting:

-

Regulatory uncertainty on climate change is a major problem for the auto sector;

-

Flexibility in manufacturing is a key factor for future profitability;

-

Investors need improved disclosure on the risks and opportunities posed by fuel prices, climate change, and other factors.

Six key factors have combined to send a strong signal to automobile companies that they must shift production to new technologies that enable them to produce vehicles that are more fuel-efficient and emit less pollution. Those six factors are:

-

Volatile gas prices. High and volatile gas prices as a result of Hurricane Katrina coupled with limited supply and rapidly rising worldwide demand.

-

Energy Security. Dramatic revisions to both the IEA’s and the EIA’s oil price forecasts, predicting rising oil prices and increasing dependence on five or six middle eastern countries.

-

Energy Independence. New calls for energy independence and ending the “addiction” to foreign oil, including the enactment of the 2005 U.S. Energy Bill to accelerate adoption of fuel efficient technologies and biofuels.

-

New Standards. New policies globally and domestically ensure that the world’s major auto markets are covered by carbon reduction or fuel economy standards.

-

Alternative Technologies. The clear emergence of hybrids as an important mid-term auto technology to produce cleaner, more fuel-efficient vehicles.

-

New Fuels. The emergence of biofuels as the alternative fuel of choice.

The findings of this paper indicate that oil prices, regulation, and new technologies, and specifically the six factors above, are pushing auto manufacturers in one direction: toward the production of cleaner, more fuel-efficient vehicles.

Jeremy Siegel (author of Stocks for the Long Run) is now lending further support that the US is in for a long term bear run. In a book to be published next year he explains that he expects baby boomers, now hitting retirement age, will start liquidating savings in the stock market to finance retirement spending. Because of the demographic bulge they represent this will put a damper of capital flows to the stock market (as well as putting strain on social security and medicare). While there is unlikely to be a great sell-off we can expect this factor to add to the downward pressure on stocks over the coming years.

Responsible Investing

All sorts of financial entities are now participating in the reinsurance market, most notably hedge funds. However one has to ask how resilient these investors will be, should there be a repeat of the 2005 hurricane season. This is the critical question and, unfortunately, the preconditions for increased hurricane activity seem to be embedded in the current cycle of increased sea temperatures. See the box below.

| Dr Robert Muir-Wood, a Lead Author for the forthcoming 4th IPCC (Intergovernmental Panel on Climate Change) Assessment Report, writes: An important milestone was reached at the end of last week in regard to the interface between the Climate System and Financial Markets. With the release of RMS's latest US and Caribbean Hurricane Catastrophe Loss models, we have confirmed that the hurricane activity measured for all forward-looking risk management applications is now higher than the long term historical average previously employed for quantifying risk. Atlantic Hurricanes generate the largest natural catastrophe insurance loss, and US & Caribbean hurricane is the most traded risk among international reinsurers and in catastrophe risk securitizations. Since our models are the most widely used in the market for setting insurance and reinsurance rates, this re-evaluation of risk -- within the insurance economy -- is the equivalent of a major dollar devaluation. The re-evaluation of risk also includes contributions from revised building vulnerabilities and the inclusion of new models of loss amplification effects -- systemic processes that expand losses for the largest catastrophes. The combination of changes in the new model has raised the annual expected loss for US insurance industry hurricane risk from USD 7 billion per year to more than USD 10 billion per year, while the 100 year loss increases from USD 70 billion to more than USD 100 billion. In effect, the former 100 year return period loss has now become the 50 year return period loss. While the 2005 season broke a number of records -- most named storms, most hurricanes, most Category (Cat) 5 hurricanes in a single season and most intense (Cat 3-5) US land-falling storms, as well as the record insurance loss -- it built on a rising baseline. Seven intense (Cat 3-5) hurricanes have made landfall in the US over the past two years -- four standard deviations higher than the long term mean. However, there has been increased hurricane activity in the Atlantic basin (including the Caribbean) since 1995, and the past two years are notable principally because high activity has now broken through to US landfall. The increase is highest for the most intense Category 3-5 hurricanes, which since 1995 have been running at more than 200% of the activity that prevailed in the 1970s and 1980s. This increase in activity and severity shows a strong correlation with raised sea surface temperatures in the main development region of the equatorial Atlantic, which themselves appear to shadow northern hemisphere temperatures, implying that there is a significant contribution from global warming. The uptick in risk in the our models means that arguably some of the costs of climate change are connecting through the economy. While reinsurers' rates are set in an open market, US insurers must deal with the rigid state-level insurance regulatory system, with elected or politically appointed officials unwilling to accept the evidence that risk has increased, or that these costs should be passed onto their electorate. It would be better if these same citizens were made better informed as to the potential link that exists between necessary increases in insurance costs and climate change. We are already seeing dislocations in the market in states such as Florida as private insurers attempt to withdraw from situations where they are unable to charge the technical rate for the risk. In surfacing issues related to rebuilding New Orleans, US government agencies have so far failed to acknowledge that the risk of storm surges from Cat 4 hurricanes with the power to overwhelm the current flood defences has significantly increased. More fundamentally, a set of international private companies, including ours, with a business model predicated on neutrality and independence may be better positioned to provide dispassionate information on risk rather than governments concerned with which interest group -- from real estate boards to consumer groups -- they are seeking not to offend. |

Investors in paper pulp producers should take note of a new report by the Centre for International Forestry Research in Indonesia. A significant number of projects financed in the last decade had no environmental assessment and may now fall foul of regulation and tougher scrutiny. A number of projects, including those of Asia Pulp and Paper and Asia Pacific Resources International came to market on the basis that they would be able to source affordable raw materials. In fact they are a long way from securing sustainable sources and their viability is thus questionable. The concerns over increasing requirements of environmental stewardship and materials availability will increase, not lessen, and investors should consider how much downside risk they have taken on.

The US organic sector grew impressively between 2000-05 with total sales topping $15bn last year, according to a new report from the Hartman Group. According to the report around 3/4 of the US population now buy organic products at least occasionally and 23% of US consumers buy organic on a regular (at least weekly) basis. Organic now commands around 2.5 % of total food sales in the US. Presenting key findings from the report at the All Things Organic summit in Chicago, Harvey Hartman noted that organic was “taking over from ‘natural’ in the US”. This was partly due to growing consumer recognition of the USDA organic seal (“while many consumers don’t know what it means they feel reassured by it”), but also because consumers had grown wary about the term ‘natural’, increasingly seeing it as a marketing tool. While "organic" will have its share of cynicism, in light of some questionable or disallowed pratices by some producers, it will continue to have significant credibility and value as a differentiator to consumers.

US Congress has passed an amendment to the Agricultural Appropriations

Bill that will increase federal funding for organic agriculture research

from $1.8 million per year to $5 million (as a reference point, eight

times that amount was spent on Bush's last inaugural party). Although

this allocation is better than nothing, organic subsidies and program

funds are ridiculously small, given the USDA's annual $90 billion budget

and the $25 billion in annual crop subsidies allocated to chemical intensive

farms and genetically engineered crops. According to the Organic

Consumers Association's National Director, Ronnie Cummins, "Since

organics represent 2.5% of all grocery sales, $15 billion in annual sales,

we deserve at least

2.5% of all USDA program monies."

In the UK, supermarket convenience stores, such as Tesco Express, are to come under the full scrutiny of the Competition Commission as it carries out its third investigation of the £5 billion-a-year grocery industry. Previous inquiries into suspected anti-competitive behaviour by the four big UK supermarket chains - Tesco, Asda, Sainbury’s and Morrison’s - have been criticised for failing to investigate the rapid growth of the supermarket C-stores. Small business groups argue that the spread of C-stores has allowed the major grocery retailers to shoe-horn themselves into the high street, where they have used supermarket tactics such as below-cost selling to draw consumers out of independents. The Office of Fair Trading, which has recommended the inquiry, says that as well as below-cost selling, the latest review will also look at the abuse of buying power and the land banks that have been built up by the big retailers. A spokesperson for Friends of the Earth, called on the Commission to: “find tough remedies that will help small shops flourish and protect farmers from bullying behaviour.”

The International Finance Corporation allocated some 11% of its total investments in fiscal 2005 to projects with a sustainable energy component, according to its latest sustainability report, Choices Matter. Read more here. The IFC - the private sector arm of the World Bank Group - has identified projects within its mainstream portfolio that have a sustainable energy component: it found 21 projects, representing $705 million of IFC investment. Of this, $221 million went directly to sustainable energy. During 2005, the IFC committed a total of $6.45 billion to 236 projects. The full report can be downloaded here.

In May Novethic presented the results of their annual study on assets under management in the French SRI market. They reported an increase of 27% in 2006, compared to 2005, with a total of 8.8 billion euros, of which 58% are for institutional investors. The report is here.

IFC's Capturing Value program invites research houses, rating firms, index providers, and similar organizations to compete for grants to encourage high-quality, long-term investment in emerging markets from pension funds and other investors worldwide.

New briefings covering SRI topics have been published by Insight Investment. The topics include corporate governance and financial performance, health and safety, the role of the board in governing corporate responsibility, climate change, voting disclosure, obesity, pesticides and environmental technology. They are available here.

MicroRate is the first rating agency specializing in the evaluation of microfinance institutions (MFIs). Its objective is to link MFIs with funding sources and in particular with international capital markets. MicroRate’s comparison tables are an useful tool for measuring the performance of MFIs. The data are verified in the field and they can be adjusted to neutralize the effect of differing accounting practices and subsidy levels.

WWF launched an umbrella fund with PhiTrust Finance, investing in companies that have a proactive commitment to environmental and social issues. Living Planet Fund - Equity is the first mutual umbrella fund invested on the international share market.

More than 25.8% percent of ConocoPhillips shareowners voted in favour of a resolution filed by Green Century Capital Management asking the company to recognize and eventually stay out of sensitive areas within the National Petroleum Reserve Alaska, particularly areas near Teshekpuk Lake. This represents the highest vote ever given by shareowners on a question of wilderness preservation.

It was disappointing to hear that Consumers International, a world collection of consumer organisations, has attacked the International Organisation for Standardisation for what it described as blocking press access to the debates at its social responsibility summit in Lisbon. The group said that it believed the action was the result of the business lobby that was 'forcing ISO' to ban the press. Richard Lloyd, Director General of Consumers International, said: "Big businesses love to tell anyone who'll listen just how socially responsible they are. Yet when it comes to media access to discussions on a global guideline for Social Responsibility, they slam the doors shut. By restricting media access to decision-making, the ISO sends a message to everybody that transparency is not an issue that needs to be taken seriously. This is an irony that won't be lost on consumers."

Venture Capital

China's government again signalled that foreign buyouts involving majority control will not be allowed in China. It announced that it will not allow a consortium investors led by Citigroup to acquire a majority stake in Guangdong Development Bank. Instead, it will require any investments to fall within the current foreign ownership limit of 19.9%. Much as they did with the recently denied or deferred Carlyle, Caterpillar and Harbin buyout deals, government regulators have informed provincial authorities who approved of the Citigroup buyout that Chinese national authorities would not approve any acquisition that gives foreign buyers majority control of a domestic Chinese company.

Global VC Insight by Ernst and Young (1.6 MB) is naturally a bit self-serving but offers some useful case studies, data and global perspective.

We'd like to draw your attention to a couple of novel sites. Ecostructure is innovating in the delivery of entrepreneurial VC services. It aims to

-

Collect cool ecological businesses and projects via their Eco-preneur Portal

-

Work with eco-preneurs to improve their presentations and business models

-

Provide financing for rapid expansion ecological business strategies via a percentage of the revenues generated from Individual and Eco-Preneur subscriptions to their website, and via their associated company, Ecostructure Capital LLC

And www.prosper.com is an online marketplace for people-to-people lending, demonstrating the jump in scope and efficency that the web can bring.

The Case for Categorizing Community Development Venture Capital as a New Asset Class by Bill Baue is a white paper by Pacific Community Ventures laying out the argument and identifying steps to promote growth in community development venture capital, such as standardizing social return metrics.

Galveston Bay Biodiesel LP, a 20+ million gallon per year biodiesel facility on Galveston Island, Texas, has raised an undisclosed amount of Series B funding from Contango Capital Management and Chevron Technology Ventures.

SolarCentury, a UK-based provider of solar energy solutions, has raised £5.5 million in new VC funding. VantagePoint Venture Partners led the deal, and was joined by return backer Scottish and Southern Energy PLC.

Last.fm Ltd, a London-based provider of an online social music network, has raised an undisclosed amount of first-round funding. Index Ventures led the deal, and was joined by angels Joi Ito, Reid Hoffman and Stegan Glaenzer.

Interest Rates and Currencies

As expected the US Fed raised base rates again at their May meeting from 4.75% to 5%. We continue to expect the rate to rise to 5.75% before year end, and if inflation becomes more pronounced in the coming quarters it may be even higher. It will be interesting to see how the higher cost of fuel will drive though to basic food prices in the US as most of US agriculture is oil based from fuelling tractors and distribution to herbicide and pesticide to fertiliser. This will become apparent in autumn and may cause a more popular reaction as consumers see price rises in daily consumption other than fuel.

The dollar slipped a bit trggered by concerns about rising inflation around the world, and because there are significant global imbalances weighing on the currency. A declining dollar appears inevitable, though it has been propped up by foreign central banks treating it as a reserve currency, and liberalisation of the rouble and yuan as well as increasing trade in Euros may lubricate its adjustment.

Commodity prices are at bubble-like levels and are due a significant correction. This seemed to be beginning with single day drops of 9% for copper and 12% for zinc. Silver and gold also came under pressure. Is it time to sell commodities?

Inflation is rising around the world. The US is obviously concerned as data showing US headline inflation rising at 5.2% annual rate. Japan seems to have turned from a deflationary environment to an inflationary one and Europe is feeling the pressure. Germany registered a leap of 6.1% in producer prices in the year to end April, the worst in almost a quarter of a century. The German statistics office cited rises of 37% in non-ferrous metals, 26% in natural gas, 7.2% in tobacco and 6.4% in meat, a breadth of range suggesting systemic pressures.

The Bank of Japan has provided liquidity to financial market players (in particular via hedge funds through the "carry trade") because of the low interest rates and the policy of maintaining stability between Yen and US dollar, the BoJ has been buying and hoarding dollars. The zero-interest policy of the BoJ may come to an end soon which will help drain liquidity from the global system.

Markets across the world are begin to face the possibility that a four-year boom may end painfully because of a seemingly abrupt growth in prices that forces central banks to jam on the breaks. It is Bernanke's misfortune in particular that he is starting his job with the global credit cycle at a peak. But all central bankers are being challenged by massive global liquidity and relatively loose money. Those economies with bubbles in the system which may burst are exposed to the most volatility - managing expectations is very difficult with inflation pushing up and the risk of certain asset classes, like housing, at risk of bursting. A broad decline in the US housing market in particular would be bad for the global economy: last year Americans fuelled demand to the tune of € 900 billion in equity withdrawals from their inflated home prices; estate agents alone made up a full 20% of the 2 million jobs created by the US economy in the past 5 years.

And if you enjoy a bit of humour, see the Borowitz report for 31 May: China Calls US Loans; Demand California as Repayment: Golden State to Become China’s East Coast

And a friend pointed out that the Columbia University Follies video "Every Breath You Take" mentioned last month has become a Cult Hit with financial media ... view the video.

Trade and FDI

The OECD warned that the global imbalances in world trade are unsustainable and must be tackled. Opening the global think tank's annual forum, Greek finance minister George Alogoskoufis said the situation posed major risks to global economic stability. Some imbalances "are clearly not sustainable and will have to be addressed in an effective manner as soon as possible," he said. His comments were echoed by the president of the European Central Bank, Jean Claude Trichet, who also addressed the OECD meeting. Unfortunately, the possibility of a productive Doha round of trade talks has all but evaporated.

Morgan Stanley's Stephen Roach comments on the massive imbalances:

By our reckoning, the disparity between the world's current account surpluses and deficits will hit an astonishing 6% of world GDP in 2006. Moreover, the deterioration is occurring at unprecedented speed. If our forecast comes to pass, this year's divergence between surpluses and deficits will be fully 50% higher than the 4% gap of 2003. And the asymmetry of the world's imbalances remains one of its most problematic characteristics: The surpluses are broadly diffused, whereas the deficits are highly concentrated; last year, the US accounted for about 70% of all the current account deficits in the world. This asymmetry underscores the precarious nature of the global disequilibrium. With the three largest surplus nations -- Japan, China, and Germany -- all hard at work in stimulating internal demand, there is a growing likelihood that their surplus saving will decline. That will put even more pressure on the funding of the largest external deficit in recorded history.

Activities, Books and Gatherings

We enjoyed BeTheChange 2006. As before we went with open minds and were pleased to be reinvigorated and stimulated by new ideas, perspectives and thoughts. The speakers were excellent with a range of personal and professional presentations that inspire. It was great to be joined on several days by friends who took time to participate in various parts of the programme. Our editor's notes are online here and will be added to by a Director's review of the gathering to be uploaded in the coming month. To give a taste of the event here are some quotes and observations:

-

3 richest people have more wealth than the bottom 600,000,000.

-

40,000 people per day die from starvation.

-

War is keeping capitalism alive.

-

In Iraq 10 civilians are killed for every combatant.

-

One drop at a time ... fills the glass.

-

At a constant density the atmosphere is 1/500 of the oceans! (reference to air pollution)

-

Advertising is founded on psychological manipulation - it appeals to the id, for 50 years it has been debasing human desires from higher aspirations to survival values – sex and consumption.

-

God put the coal and oil underground for a reason – to give us a climate

-

As knowledge grows, so the interface with the unknown grows!

-

$ 14,000/second spent on security

-

Dream like you live forever. Live like you'll die tomorrow.

May was fun and productive. Meetings with new acquaintances and BTC were fun and, because wet weather was a good excuse not to be in the garden, the office was productive. The weather has been a bit late this year, which gave a bit of a breather and has meant that bluebells and rhododendrons are still blooming at the end of May. We are very lucky.

Getting in to Maverick! by Ricardo Semler has been enjoyable. He offers smart, tested methods of applying open management. And his story, which is woven throughout and holds the reader's attention is an unusual and enjoyable tale. Definitely recommended for entrepreneurs, managers and owners.

Dipping back into Emotional Intelligence by Daniel Goleman is always stimulating and edifying. It offers alot of detail about human thought processes and from a perspective traditionally neglected. It makes one realise that education needs a whole new dimension, that of emotional skills, to develop people. It would not require a huge investment but is evidently so important. We see examples everyday of people who should know better behaving at primitive levels. On a national scale it is the wealthiest nations adopting infantile belligerence to achieve selfish, and potential self-defeating, aims. Emotional Intelligence is recommended for all.

Pratchett is a master. Visiting an old bookstore in London a specialist there said a reason Pratchett is different among writers is that he is always "straight", his characters are true to character. This resonates strongly with me and is a sound rationale for my love of his style. I think the reason some people can not get comfortable with him is because they see aspects of themselves in his fantastic tales - I know my weaknesses are highlighted by his characters. The Fifth Elephant is a tale of diplomacy and criminal investigation which also plays with the problem of prejudice. I like the quote "muck and gold come from the same hole" to describe how siblings can be quite different. I could not work out why it was called the Fifth Elephant, except to realise that it is a reference to the Fifth Element (movie with Bruce Willis), but then I read The Truth in which he provides the last piece of the puzzle: "The world is made up of four elements: Earth Air, Fire and Water. ... There's a fifth element, and generally it's called Surprise." You'll have to read the book to get the big picture though.

The Truth is one of my favourites, as you might expect by its title, although it is certain that you can tell the truth without being honest. It lends pertinent insight to the dangers of privilege: defining a criminal "as anyone with less than a thousand dollars a year" or treating justice "like coal or potatoes. You ordered [it] when you needed it." And relevant to concerns expressed in Geopolitics and elsewhere in this month's newsletter, "A lie will go around the world before the truth has got its boots on." And if you enjoy stretching your philosophy: "Have you heard the theory that there is no such thing as the present? Because if it is divisible, then it cannot be the present, and if it is not divisible, then it cannot have a beginning which connects to the past and an end that connects to the future? The philosopher Heidehollen tells us that the universe is just a cold soup of time, all mixed up together, and what we call the passage of time is merely quantum fluctuations in the fabric of space-time." Pratchett probably had particular fun with The Truth because it is a story of journalism, which is a business he was once involved with.

A friend of ours has recently published a book reviewing some of the key corporate failures in recent past. The conclusion that greed and arrogance at the top is the principal cause will not be news to SRI advocates. Greed and Corporate Failure: The Lessons from Recent Disasters offers chapter case studies on:

Barings and Allied Irish Bank: Lessons Ignored

Enron: Paper Profits, Cash Losses

WorldCom: Disconnected

Tyco: Greed, Hubris and the $6000 Shower Curtain

Marconi: Establishment to Wunderkind to Basketcase

Swissair: Crashed and Burned

Royal Ahold: Shopped till he Dropped

Parmalat: Milking the System

And for an alternative view of news,

you might find a browse through CounterPunch

worthwhile.

This report has been prepared for information purposes and is not an offer, or an invitation or solicitation to make an offer to buy or sell any securities. This report has not been made with regard to the specific investment objectives, financial situation or the particular needs of any specific persons who may receive this report. It does not purport to be a complete description of the securities, markets or developments or any other material referred to herein. The information on which this report is based, has been obtained from publicly available sources and private sources which may have vested interests in the material referred to herein. Although GRI Equity and the distributors have no specific reasons for believing such information to be false, neither GRI Equity nor the distributors have independently verified such information and no representation or warranty is given that it is up-to-date, accurate and complete. GRI Equity, associates of GRI Equity, the distributors, and/or their affiliates and/or their directors, officers and employees may from time to time have a position in the securities mentioned in this report and may buy or sell securities described or recommended in this report. GRI Equity, associates of GRI Equity, the distributors, and/or their affiliates may provide investment banking services, or other services, for any company and/or affiliates or subsidiaries of such company whose securities are described or recommended in this report. Neither GRI Equity nor the distributors nor any of their affiliates and/or directors, officers and employees shall in any way be responsible or liable for any losses or damages whatsoever which any person may suffer or incur as a result of acting or otherwise relying upon anything stated or inferred in or omitted from this report.